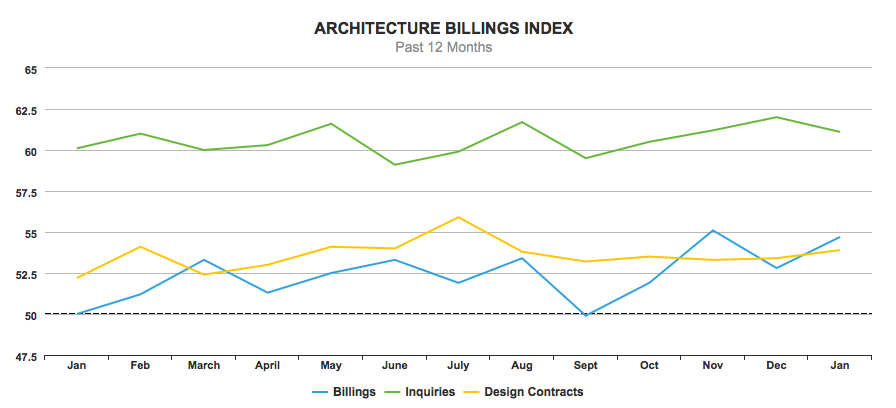

The AIA's monthly Architecture Billings Index (ABI) came in at a score of 54.7 in January—the highest score seen during the first month of the year since 2007. The ABI is a leading economic indicator of construction activity in the U.S., and reflects a nine- to 12-month lead time between architecture billings and construction spending nationally, regionally, and by project type. A score above 50, as seen this month, represents an increase in billings from the previous month, while a score below 50 represents a contraction.

Healthy demand for design services continued in January, with national billings reaching a score of 54.7. January's reading is 1.9 points higher than December's score of 52.8. However, new project inquiries—considered to be the most reliable indicator of future billings—decreased 0.9 points in January to a score of 61.1, indicating that billings could ease in February.

“Healthy conditions continue across all sectors and regions except the Northeast, where firm billings softened for the second consecutive month,” said AIA chief economist Kermit Baker, Hon. AIA, in a press release. “With strong billings and healthy growth in new projects to start the year, firms remain generally optimistic about business conditions for the next several months.”

Design contracts remained relatively unchanged in December, with a score of 53.9—a 0.5-point increase from December's score of 53.4. This portion of the index has has fluctuated less than one point for the past five months, but stayed above the 50-point threshold every month last year—a sign that momentum is strong in the market, despite small fluctuations in pace month-to-month.

Regional billings, which, unlike the national score, are calculated as a three-month moving average, increased in three of four regions in January. The Northeast was the only region to post a lower score than a month prior, dropping 2.1 points from December's score of 49.4, to a score of 47.3. With a score below 50, the Northeast is the only region where design services decreased last month; all other regions posted a score above 50. Demand for design services increased most significantly in the Midwest, rising 1 point from December's score of 53.8, to a score of 54.8. Billings also increased in the South (55.3) and West (56.2) regions during January, with 0.5- and 0.4-point increases in score, respectively, than a month prior.

Demand for residential design services was strongest for the third consecutive month, with a score of 56.0—a 0.2-point increase from December's score of 55.8. The residential sector was the only category of the four building sectors included in the index to experience increase demand for design services in January. All sectors posted scores above 50, however, marking the 12th consecutive month of growth. Demand in the institutional sector (52.5), commercial/industrial sector (53.3), and mixed-use sector (50.1) dipped less than a point in January, reporting 0.3-, 0.5-, and 0.7-point decreases in billings, respectively. (Results of sectors are also calculated as a three-month moving average.)