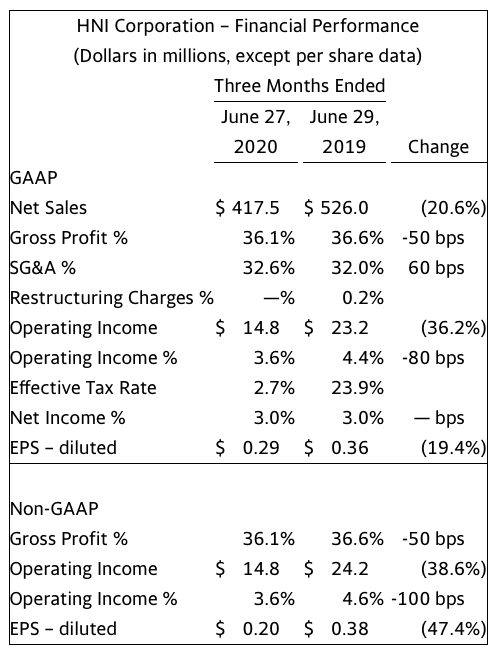

HNI Corporation today announced sales for the second quarter ended June 27, 2020 of $417.5 million and net income of $12.6 million. GAAP net income per diluted share was $0.29, compared to $0.36 in the prior year. Non-GAAP net income per diluted share was $0.20, compared to $0.38 in the prior year.

Second Quarter Highlights

The Corporation delivered solid profits and increased second quarter operating cash flows by $20 million or 49 percent versus the prior year despite pandemic related top-line pressures.

Residential Building Products segment operating profit increased, and segment operating margin expanded on a year-over-year basis in the second quarter 2020.

Workplace Furnishings segment generated second quarter 2020 operating profit of nearly $8 million, despite a 25 percent year-over-year contraction on the top line.

Quarter-ending debt levels were $183 million, equal to a gross leverage ratio of approximately 0.8x. Liquidity, as measured by cash and borrowing availability, at the end of the second quarter was $392 million.

"Our members did a great job of managing through challenging second quarter conditions. We aggressively managed costs and drove productivity—offsetting much of the impact from lower volumes. Our teams stayed focused on our customers—generating and seizing market opportunities. The strength of our strategy, including our diverse revenue streams, price point breadth, channel reach, and lean operating model, along with the dedication of our members, helped demonstrate again what makes HNI unique," stated Jeff Lorenger, Chairman, President, and Chief Executive Officer.

Salary adjustments

Compensation for HNI members and Board of Directors are being restored to levels existing prior to the reductions announced on April 22, 2020.

"Our members responded in an outstanding manner to this environment, and I am pleased we are able to take this action 60-90 days earlier than we originally anticipated," continued Mr. Lorenger.

Debt Level Update

As of June 27, 2020, the Corporation’s net debt totaled $157 million (as defined as gross debt of $183 million less cash and cash equivalents of $26 million). At the end of the quarter, the Corporation had $366 million of borrowing capacity under its existing $450 million credit facility. On a gross leverage basis, the quarter-ending level of 0.8x remains well below the Corporation’s debt covenant of 3.5x.

"We generated strong free cash flow in the quarter and further enhanced our already strong balance sheet. We have the financial strength and cost structure to successfully weather this crisis for a prolonged period," said Mr. Lorenger.

Second Quarter Summary Comments

Consolidated net sales decreased 20.6 percent from the prior-year quarter to $417.5 million. On an organic basis, sales decreased 21.2 percent. The impact of acquiring residential building products distributors increased sales $2.9 million compared to the prior-year quarter. A reconciliation of organic sales, a non-GAAP measure, follows the financial statements in this release.

Gross profit margin decreased 50 basis points compared to the prior-year quarter. This decrease was primarily driven by lower volume, partially offset by price realization and net productivity.

Selling and administrative expenses as a percent of sales increased 60 basis points compared to prior-year quarter due to lower volume, partially offset by lower core SG&A spend and net productivity.

Non-GAAP net income per diluted share was $0.20 compared to $0.38 in the prior-year quarter. The $0.18 decrease was primarily due to lower volume, partially offset by lower core SG&A spend, net productivity, and price realization.

Non-GAAP EPS in the current quarter includes an effective tax rate of 32.5 percent, compared to a GAAP tax rate of 2.7 percent. The higher non-GAAP tax rate is related to timing of the tax impact from one-time charges recorded in first quarter 2020.

Workplace Furnishings net sales decreased 24.8 percent from the prior-year quarter to $308.1 million.

Workplace Furnishings GAAP operating profit margin decreased 210 basis points versus the prior-year quarter. On a non-GAAP basis, segment operating margin decreased 230 basis points year-over-year driven by lower volume, partially offset by net productivity, lower core SG&A spend, and price realization.

Residential Building Products net sales decreased 6.1 percent from the prior-year quarter to $109.4 million. On an organic basis, sales decreased 8.6 percent. The impact of acquiring building products distributors increased sales $2.9 million compared to the prior-year quarter.

Residential Building Products operating profit margin expanded 160 basis points, driven by price realization, lower variable compensation, lower core SG&A spend, and net productivity, partially offset by lower volume and unfavorable mix.

Concluding Remarks

"The HNI culture remains the foundation for our success. Together, our members, dealers, suppliers, and communities will continue to overcome the challenges presented by this crisis.

Pandemic-related uncertainty continues to limit visibility and our ability to provide guidance. However, we are seeing a seasonal uptick in sales and do expect third quarter sales and profit to track ahead of second quarter 2020 levels. We have demonstrated we can adapt our cost structure quickly, and our balance sheet is strong. More importantly, we have developed new and better ways to operate our businesses that will serve us well in the future," Mr. Lorenger concluded.