The AIA's monthly Architecture Billings Index (ABI) came in at a score of 51.0 in March, marking the sixth consecutive month of gains. The ABI is a leading economic indicator of construction activity in the U.S., and reflects a nine- to 12-month lead time between architecture billings and construction spending nationally, regionally, and by project type. A score above 50, as seen this month, represents an increase in billings from the previous month, while a score below 50 represents a contraction.

While March's reading of 51.0 is a 1-point dip from February's score

of 52.0, the fluctuation only indicates a slower rate of business activity during the month, though the industry continues to grow. New project inquiries—which AIA economists consider to be the most reliable indicator of future billings—decreased 4.3 points in March to a score of 58.1, indicating that demand for design services could be softer next month.

“New project activity coming into architecture firms continues to grow at a solid pace. As a result, project backlogs—in excess of six months at present—are at their highest post-recession level,” said AIA chief economist Kermit Baker, Hon. AIA, in a press release. "Business remains strong in the South and West, and firms with a residential specialization continue to set the pace.”

In March, design contracts received a score of 51.5—a 3-point decrease from February's score of 54.5. For the past six months, this portion of the index had fluctuated within a range of less than a point. Despite last month's significant change, design contracts continue to fall above the 50-point threshold—as they have every month in the last year—a sign that momentum is strong, despite small month-to-month fluctuations.

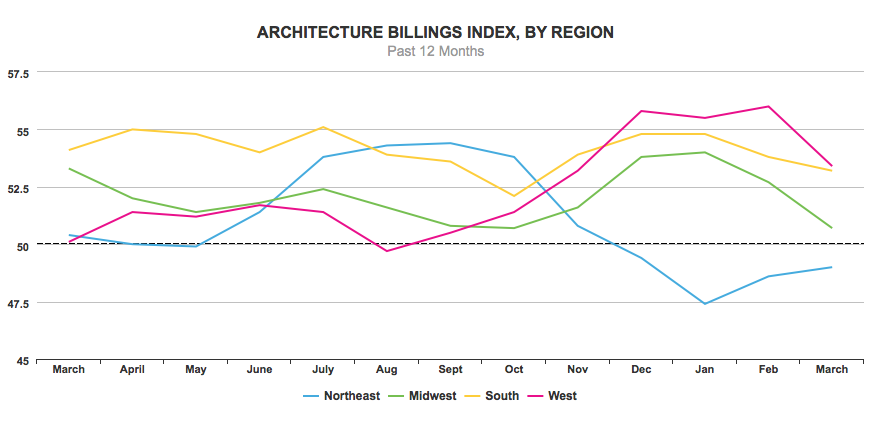

The scores for regional billings—which, unlike the national score, are calculated as a three-month moving average—decreased in three of four regions during March. The South (53.2) saw a minor 0.6-point decrease in billings, while the the pace of design activity slowed more significantly in the Midwest (50.7) and West (53.4), with billings dropping by 2.7 points, and 2.6 points, respectively. Despite the month-to-month decrease in billings, business activity has been strongest in the West and South region for the past five months. The Northeast was the only region to report an increase in billings last month, but the 0.4-point increase in billings to a score of 49.0, making it the only U.S. region with a score below 50. March marks the fourth consecutive month of contraction in the Northeast, and the fourth consecutive month that the Northeast was the only region not growing.

Billings decreased in three of four sectors in March, but the institutional sector was the only sector to show contraction, dropping 2.1 points to a score of 49.7. All other sectors posted billings scores above 50, indicating growth. With a 0.4-point increase in billings to a score of 53.1, the commercial/industrial sector was the only sector to see a higher rate of business activity compared to a month prior. Billings in the mixed-use sector saw a minor 0.1-point dip in March, to a score of 51.1. For the fifth consecutive month, demand for design services was strongest in the multifamily residential sector (53.4), despite a 1.1-point decrease in billings month-to-month. (Results of sectors are also calculated as a three-month moving average.)